Unlock the future of mobility

Opportunities and threats facing financial services providers in the mobility revolutionDive into the latest trends shaping the mobility industry with our new report developed in collaboration with Corporate Value Associates. Gain valuable insights and strategies from global industry leaders to stay ahead in the rapidly evolving landscape.

Most recent News & Articles

CLV: Gaming insights are helping banks pinpoint key long-term customers

At an online event hosted by Qorus Digital Reinvention Community and marketing firm Numberly, Zachery Anderson, NatWest’s Chief Data and Analytics Officer, discussed how CLV is changing how banks are connecting with their customers.

OCBC introduces program to aid women entrepreneurs

The programme offers tailored financing solutions, educational workshops, and networking and mentorship opportunities.

Allianz Partners takes top prize for MAvalue app at Qorus Reinvention Awards – Europe 2024

Last month at the Qorus Reinvention Awards – Europe 2024, Allianz Partners won the Operational Efficiency gold award for MAvalue,...

Innovation Masters: Banks at the forefront of women's business empowerment

A selection of innovative projects empowering female entrepreneurship, submitted for the Qorus Banking Innovation Awards in recent years by KCB,...

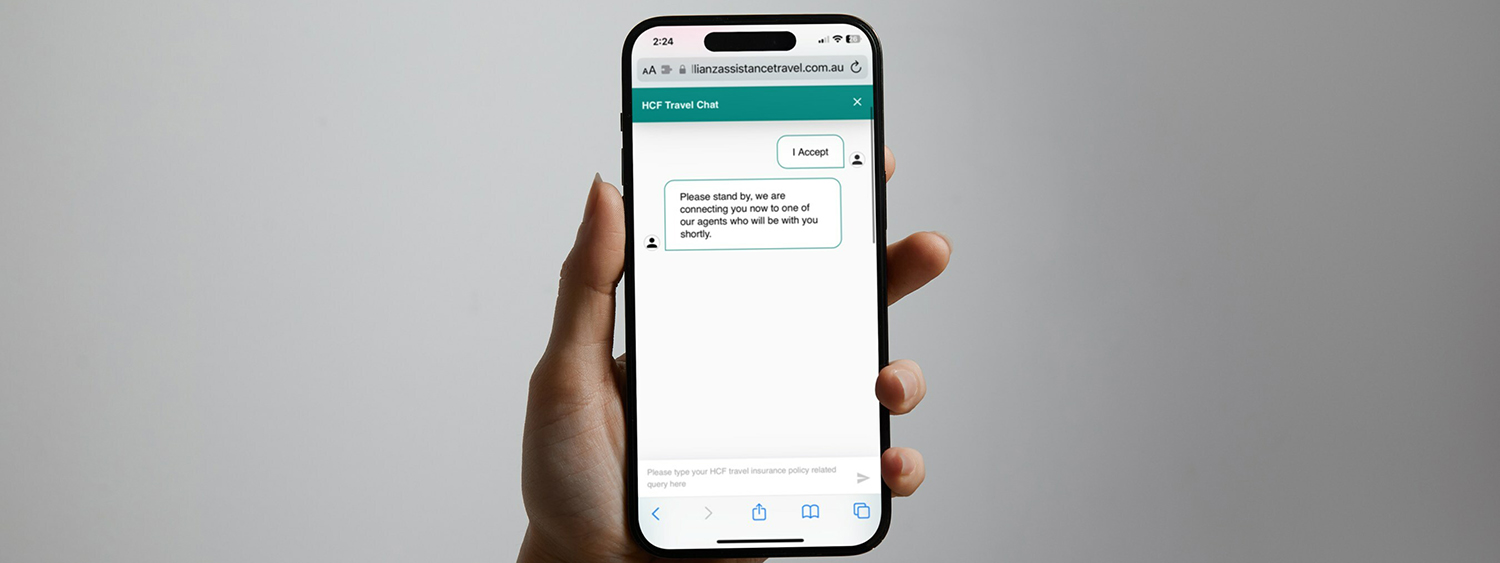

Allianz Partners introduces instant online chat for HCF travel insurance customers

This pioneering service furnishes HCF members with real-time support for their travel queries, broadening the avenues through which customers can...

Lemonade expands homeowners insurance offering in France

Lemonade, the digital insurance company, has expanded its offerings in France by introducing Homeowners insurance in partnership with BNP Paribas...

MetLife Pet Insurance partners with the Association of Animal Welfare Advancement

MetLife Pet Insurance and the Association of Animal Welfare Advancement (AAWA) have joined forces to address pet owners' challenges in...

Most recent Studies & Reports

Driving forces: The interplay of financial services and the EV sector

The financial services sector and the electric vehicle (EV) sector are two dynamic realms undergoing a significant transformation in today's...

A bancassurance breakthrough: Nurturing SME relationships through customized insurance products

In this paper, we outline the opportunity bancassurance presents to banks, as well as the key considerations that should be...

Innovation Radar: Reinvention Awards Europe winners 2024

Discover the most innovative projects from banks and insurance companies in Europe.

Unleashing SME banking potential with embedded finance: Simplifying financial services to create unprecedented convenience for SMEs

In this paper, we will unravel the key challenges that banks need to address to not only navigate the upcoming...

Latest innovations

New Ireland Assurance Advisor Portal

Executive Summary: The challenge we set for ourselves was ambitious and required a complete transformation of our ways of working,...

New Ireland Assurance Customer & Broker Portal

The challenge we set for ourselves was ambitious and required a complete reimagining of the customer experience. Traditionally financial advisors,...

AIA One--Reimagining the sales agent experience at AIA Thailand

At AIA, we are leveraging Technology, Digital and Analytics (TDA) across our business as we transform into a customer-centric, digital...

Walaa Modernize Core Insurance Platform

Walaa is a top tier insurance company in Saudi Arabia, which provides +60 products and services offering, has been experiencing...

Join the Qorus

Today, Qorus is a catalyst for reinvention for our financial services members by helping them to go further, be faster and work together.

Forthcoming events

Embracing Payments Composability: Blueprint, Best Practices and Learnings

Join this webinar to understand what are the key characteristics of composable payments platform, why it is imperative for banks to at now and how can banks transition from their current state to a future-ready position.

Cybersecurity: The role of the banks and insurance

Examine symbiotic relationships between financial institutions and embedded cybersecurity insurance, emphasizing collaborative efforts against digital risks and cyber threats. This session organized with our partner Allianz Partners, will explore the complexities of cybersecurity within the financial services industry and discuss effective cyber risk management practices. Invited experts will examine how...

Reinvent Forum Lisbon

Reinvent Forum Lisbon - is dedicated to the digital transformation influencing the insurance sector. Our event brings together industry leaders, experts, and innovators to delve into the latest trends and strategies for enhancing customer satisfaction through innovative digital endeavors. Attendees can expect profound insights into the evolving landscape of insurance.

Electric vehicle charging

Future position of insurance in mobility will be shaped by ongoing technological advancements, changing consumer behavior, and evolving regulatory frameworks. One of the key roles of insurance in mobility will be to provide coverage for new and emerging risks associated with the use of new technologies, such as autonomous vehicles...

Climate change and insurance gap

Climate change intensifies the insurance gap, driving a surge in extreme weather events and economic losses. Join our online event to collaborate on building a more resilient future in the face of climate change.

We help banks and insurers to reinvent themselves to thrive.

Further

Further

We curate inspiring and innovative projects, technology and ideas so individuals, teams and organisations can collectively create the future of financial services.

Faster

Faster

We’re a catalyst for reinvention, improving revenue generation, creating efficiencies, redefining customer experiences and forming profitable relationships.

Together

Together

We're a neutral space where members unite to share, learn and collaborate, thinking freely to solve problems through an ecosystem of unique, specialist communities.